Colorado first in nation on rising insurance costs; Why insurance costs are the newest affordability challenge.

Bob Engel

As a real estate professional with over thirty-five years of national real estate experience, Bob has the strong industry knowledge rarely found in re...

As a real estate professional with over thirty-five years of national real estate experience, Bob has the strong industry knowledge rarely found in re...

Why Rising Insurance Costs Are Becoming Colorado's Newest Affordability Challenge

For years, conversations about housing affordability have focused on home prices and mortgage interest rates.

Today, another expense is quietly becoming one of the largest monthly costs facing Colorado homeowners. Insurance.

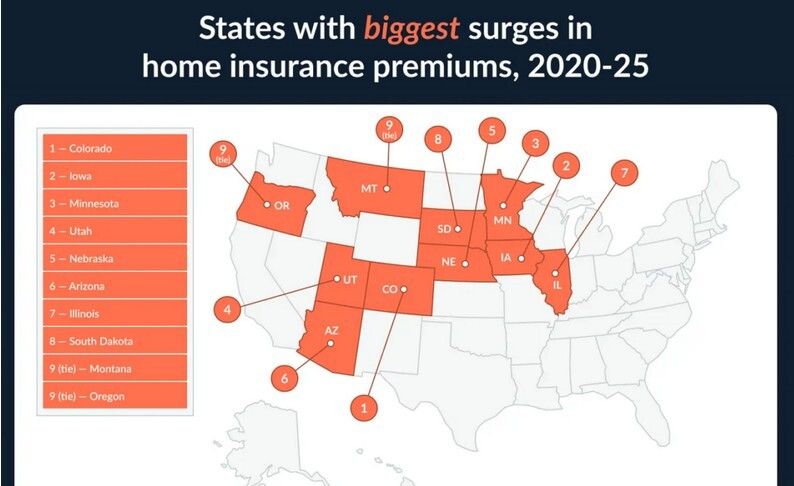

Colorado now leads the nation in the rate at which homeowners insurance premiums are increasing. Since 2020, premiums have roughly doubled for many homeowners, dramatically increasing the true cost of homeownership.

While Colorado isn't yet the most expensive state overall—that distinction still belongs to hurricane-prone states like Florida and Louisiana—our rate of increase is among the fastest in America.

The Hidden Cost That's Changing Housing Affordability

Many buyers carefully calculate:

- Purchase Price

- Mortgage Payment

- Property Taxes

- HOA Dues

Increasingly, they're discovering a fifth expense that's growing even faster:

Homeowners Insurance

Just a few years ago, insurance represented a relatively small portion of a homeowner's monthly housing payment.

Today, insurance premiums can add hundreds of dollars every month to the cost of owning a home—effectively reducing affordability just as much as a higher mortgage payment.

For many first-time buyers already stretching to qualify, this additional expense can mean qualifying for a smaller loan—or delaying homeownership altogether.

Colorado Didn't Get Here Overnight

Several major forces have collided simultaneously.

1. More Severe Weather

Colorado experiences some of the nation's highest concentrations of hail damage. Roof replacements alone have become dramatically more expensive as building materials and labor costs continue climbing. Every major hailstorm generates thousands of insurance claims across the Front Range.

2. Wildfire Risk

The Marshall Fire permanently changed how insurers evaluate risk throughout Colorado. Entire suburban neighborhoods once considered relatively low-risk are now priced differently by insurance companies. Wildfire exposure is no longer viewed as exclusively a mountain-community problem.

3. Rising Construction Costs

Insurance doesn't replace what your house was worth. It replaces what it costs to rebuild. Construction costs have increased dramatically since 2020 due to:

- Labor shortages

- Higher lumber prices

- More expensive roofing systems

- Updated building codes

- Material inflation

As rebuilding becomes more expensive, insurance premiums naturally follow.

4. More Homes in Higher-Risk Areas

Colorado continues expanding into foothills and the wildland-urban interface. Every new home built in these higher-risk areas increases insurers' overall exposure, affecting pricing across much of the state.

The Affordability Domino Effect

Higher insurance costs don't just affect homeowners. They ripple throughout the entire Colorado economy.

Home Buyers:

Higher monthly payments reduce purchasing power. A buyer qualifying for a $700,000 home two years ago may now qualify for substantially less after factoring today's insurance costs.

Home Sellers:

Higher ownership costs can reduce buyer demand. Some buyers now compare insurance quotes before making offers, particularly in wildfire-prone neighborhoods. Insurance has quietly become another negotiating factor alongside mortgage rates and HOA fees.

Renters

Landlords face higher insurance costs too. Those increased expenses often find their way into future rent increases. Even renters who never own a home ultimately pay part of the insurance burden.

HOA Communities

Condominium associations and homeowner associations across Colorado are seeing significant increases in master insurance policies. The result? Higher HOA dues. Special assessments. Reduced reserve funds. These increases affect thousands of Colorado homeowners—even if they've never filed an insurance claim.

Local Businesses

Commercial insurance costs are climbing as well. Restaurants. Retail stores. Medical offices. Manufacturers. Construction companies. Those increased operating expenses often translate into higher prices for consumers. Insurance inflation becomes general inflation.

Colorado's Insurance Market Is Changing

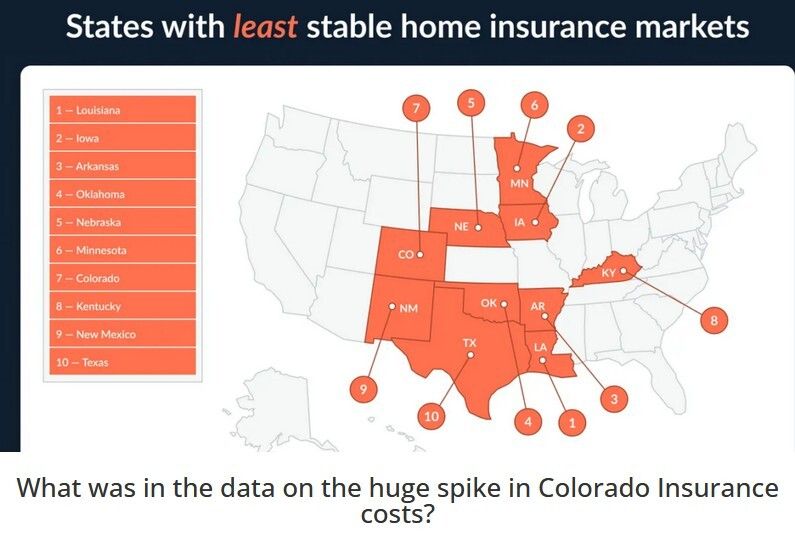

Some national carriers have reduced their exposure in Colorado. Others have tightened underwriting standards. Some neighborhoods now have fewer insurance choices than they did only a few years ago.

When competition decreases, prices generally increase. Colorado recently launched its FAIR Plan to provide coverage for property owners who cannot obtain insurance through the traditional market, although it is intended as an insurer of last resort rather than a replacement for the private insurance market.

What Buyers Should Do

Today's buyers should include insurance shopping early in the purchasing process—not after they're already under contract. Before making an offer:

✓ Obtain insurance quotes

✓ Ask about prior claims

✓ Review roof age

✓ Understand wildfire exposure

✓ Evaluate replacement costs

These steps can prevent unpleasant surprises before closing.

What Sellers Should Do

Sellers can improve marketability by being proactive. Consider:

- Maintaining roofs

- Completing deferred maintenance

- Providing recent inspection reports

- Demonstrating mitigation improvements

- Offering a home warranty

The more confidence buyers have in a property's condition, the easier it becomes to justify both price and insurance costs.

Looking Ahead

Colorado isn't likely to see insurance premiums return to pre-2020 levels anytime soon. However, homeowners who invest in mitigation—impact-resistant roofing, wildfire hardening, updated electrical systems, and other resiliency improvements—may benefit as insurers increasingly reward lower-risk properties.

State leaders are also pursuing strategies intended to reduce future premiums through home hardening, wildfire mitigation, and insurance market reforms, though the long-term effectiveness remains to be seen.

One thing is becoming increasingly clear: Housing affordability is no longer determined solely by home prices and mortgage rates.

Insurance has become a major part of the affordability equation—and one every Colorado buyer and homeowner should understand.

PrimeTime Insight

Colorado's housing market is evolving. While moderating home prices and increased inventory are creating opportunities for buyers, rising ownership costs—including insurance, property taxes and HOA dues—are becoming the next major affordability challenge.

Understanding these costs before buying—or proactively addressing them before selling—can make the difference between a smooth transaction and an expensive surprise.